2023 saw the continued advancement of Open Banking, the innovative technology that provides third-party financial service providers access to consumer banking, transaction, and other data from banks and non-bank institutions through application programming interfaces (APIs), which has evolved from a frequently cited buzzword to a powerful force in the financial sector. The coming year is expected to be a breakout year for Open Banking, with its potential influencing a broad spectrum of payment-related services.

This includes the growing rise of Account-to-Account (A2A) transfers, the enhancement of Real Time Payment (RTP) processes in the EU, the widespread adoption of FedNow in the USA, and the application of Open Banking methodologies in diverse regions such as Southern America and the Indo-Pacific. Combined, these developments collectively signal 2024 as the year when the full, global potential of Open Banking will be realized.

Open Banking is often the technological solution behind many alternative payment methods (APMs), and this article is part of our ongoing series which has gone in-depth, continent by continent, on the most popular methods consumers around the world like to transact in, from Asia, to South America, to the European Union, and then Africa. We also explored other solutions in our APM series, such as the continued popularity of cash-based payment systems.

Empowering More Businesses Through Account-to-Account Payments

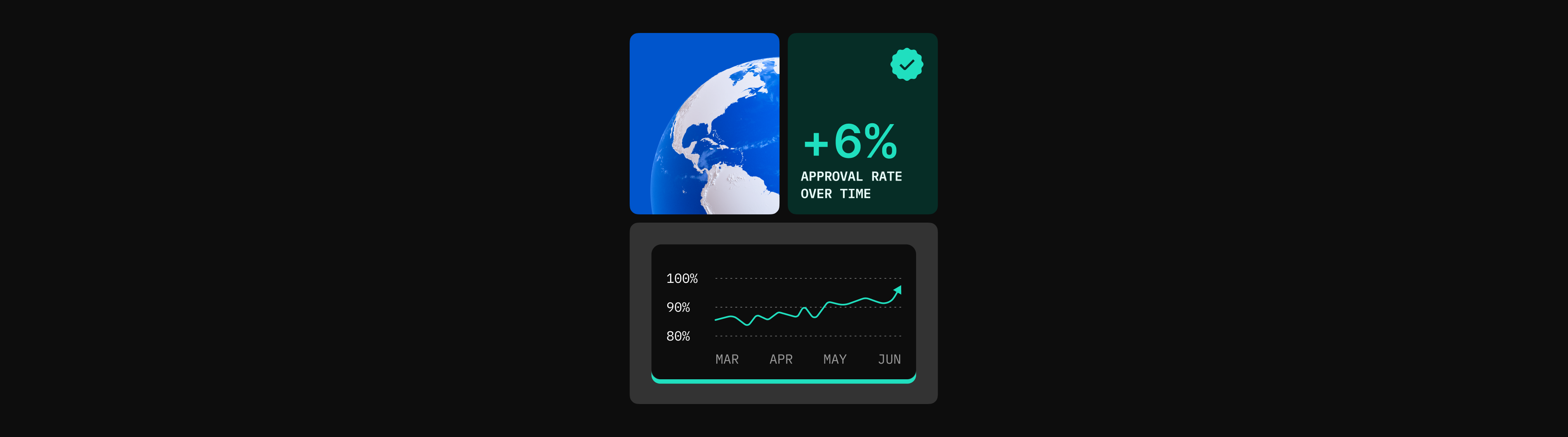

One key area Open Banking solutions are set to rise is Account-to-Account (A2A) payments. Open Banking APIs, which serve as secure gateways for third-party providers to access financial data with customer consent, are increasingly enabling seamless connections between bank accounts, facilitating direct money transfers without the need for middlemen or intermediaries. Eliminating the latter has allowed those who harness Open Banking transfers to save approximately 2-3% per transaction, according to PwC. This represents a substantial cost-saving, particularly when considered at scale.

A2A payments streamline money movement directly between bank accounts and are increasingly utilized in Person-to-Person (P2P), Person-To-Business (P2B), and Business-to-Business (B2B) transactions. Real-time Payments (RTP), a subset of A2A, facilitate transfers outside card networks in under 10 seconds.

Moving into 2024, the integration of Open Banking across more financial institutions is expected to elevate A2A and RTP transactions to new heights. The US Federal Reserve’s launch of FedNow in summer 2023, which facilitates instant payments for American households and businesses, is expected to be adopted by an increasing number of banks in the US. Meanwhile, in November this year, the two co-legislators of the EU, the Council and Parliament, reached a provisional agreement on the Instant Payments proposals, which would obligate PSPs in the region to facilitate euro payment transfers within a time period of ten-seconds.

Overall, this technology promises to enhance how businesses, both large and small, manage their financial transactions. It also opens up new markets for online businesses, particularly in the international arena, by making international payroll, vendor payments, and revenue collection transactions as simple as domestic money movement.

A Decade of Progress Preparing Open Banking for Takeoff

Open Banking's roots trace back over a decade, but only recently has the technology matured for widespread adoption. The groundwork laid for its 2024 surge includes:

- Regulatory Foundations: Initiatives like PSD2 in Europe have been critical, mandating open APIs for banks and fostering an ecosystem for third-party service development. With PSD3’s proposals, there's a move to set more stringent standards for data access interfaces, that will further ensure secure consumer protections. Read more in our article on PSD3’s proposals here.

- Technological Evolution: Financial institutions have overhauled their tech infrastructure, aligning with Open Banking as a strategic and business imperative. This shift involved partnerships with FinTechs to improve services and upgrade their legacy systems.

- Consumer Adoption: Steadily, digital-savvy users are recognizing Open Banking's conveniences in both speed and cost saving. This awareness is expected to rise in 2024 and subsequent years.

Beyond payments, Open Banking APIs have further enhanced FinTech offerings in personalized fund management and spending analytics. These tools assist in budgeting and planning, demonstrating Open Banking's versatility beyond transactions. For a holistic view of Open Banking’s innovations, outside of payments, this Financial Times article outlines its most impressive applications.

Looking Ahead: What 2024 has in store for Open Banking

As we look forward to 2024, Open Banking technology is expected to surpass its current scope, impacting populations around the world. From the EU’s implementation of its proposed Instant Payments methods, to the expansion of FedNow in the US, to the increased dominance of Brazil’s A2A alternative payment method powered PIX, and the rise of real-time cross-border A2A payment initiatives in the Indo-Pacific region with projects such as the Bank of International Settlements’ led Project Nexus, which seeks to standardize ways for various instant payment systems around the world to communicate with each other, consumers and businesses will increasingly come to rely on Open Banking powered payments.

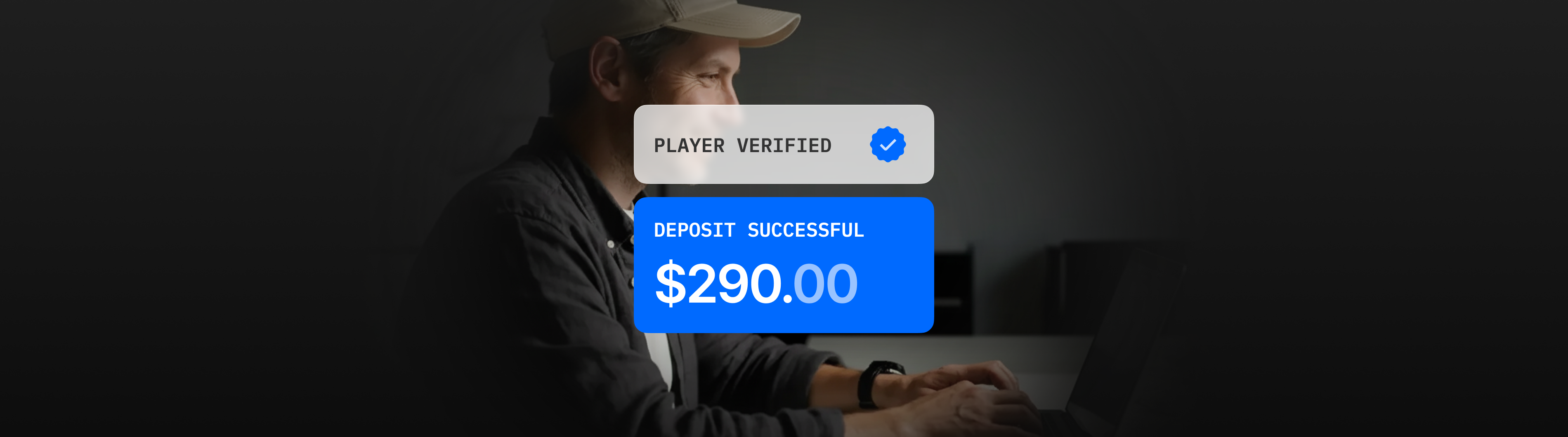

Praxis is committed to systematically integrating additional Payment Initiation Service Providers (PISPs) to broaden support for an extensive range of banks in Europe and worldwide. Simultaneously, we are implementing intelligent recovery features that facilitate seamless interactions between cards and open banking, thereby reducing merchant costs and increasing approval rates.

For businesses who would like to explore how best to incorporate Open Banking solutions in their payment operations, Praxis Tech actively integrates these solutions across our product offerings and feature suite. From supporting Open Banking powered payment methods in our Cashier, to facilitating its use in a Decline Recovery feature that boosts transaction approval rates by cascading to Open Banking protocols if a card transaction is not initially improved, get in touch to learn more and see a demo.